By Bryon Bratcher

Almost every conversation I have with a general counsel or a legal operations leader about artificial intelligence arrives, sooner or later, at the same fork in the road. Do we buy an off-the-shelf AI tool, or do we build our own? It is presented as a strategic choice, a lane you have to pick, and the assumption underneath it is that buying and building are competing uses of the same finite budget. A dollar spent on one is a dollar taken from the other.

I have come to believe that this is the wrong question, and the market data increasingly suggests the same.

The framing made sense in an earlier era of legal technology. In those days, building genuinely meant a multi-year, seven-figure custom software project, while buying meant signing a license and hoping the vendor’s roadmap eventually caught up to your needs. The two really were alternatives, and choosing between them was a meaningful decision with real trade-offs. Generative AI has quietly dissolved that trade-off. Because the underlying models are a shared foundation that any organization can access, the cost and time required to build something proprietary on top of them has collapsed. Building is no longer the opposite of buying. It is increasingly what you do after you buy.

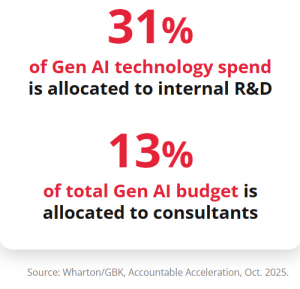

The most useful evidence I have seen for this comes out of Wharton’s 2025 enterprise AI adoption study, which found that roughly thirty-one percent of generative AI technology spend is now being directed toward internal research and development, the work of building proprietary, customized capabilities in-house. It is worth pausing on what that number does and does not mean. It does not mean that organizations have stopped buying tools. The same research shows enterprise AI budgets rising broadly, with the large majority of leaders planning to increase what they spend on third-party tools in the year ahead. Commercial adoption remains the foundation. What the thirty-one percent tells us is that a serious and growing share of the budget is flowing toward building, and that this is happening alongside the buying rather than instead of it. The spending data is simply catching up to a decision the leading organizations have already made.

This pattern echoes something we have written about before. There is a familiar instinct, when a powerful general-purpose tool becomes available, to assume it will make specialized solutions unnecessary. Why build anything when you can buy a capable product off the shelf? But that instinct misreads where competitive advantage actually comes from. Widely available tools raise the floor for everyone. They are becoming table stakes, and that is genuinely good news, because it means every legal team can get productive on the routine work quickly. What they do not do, almost by definition, is differentiate you, because the firm down the street is licensing the very same product. Differentiation comes from what you build on top of that foundation: the workflows shaped by how your organization actually operates, the institutional knowledge encoded into a system, the proprietary layer that reflects your specific data, your specific risk posture, and your specific way of doing the work.

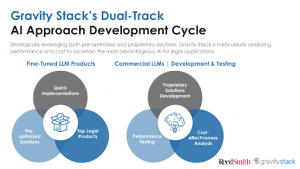

This is not new thinking for us. Back in 2023, well before the spending data and the broader market caught up, we were already describing what we called a dual-track AI approach. On one track, we evaluate and deploy the best pre-optimized, commercially available legal products, the tools that deliver speed and quick wins. On the other, we develop proprietary, fine-tuned solutions for the problems where a customized build delivers an edge that no off-the-shelf product can match. The discipline that holds the two tracks together is constant, unsentimental measurement of performance and cost, letting the use case decide which track wins for a given problem rather than letting ideology or a vendor’s sales pitch decide it in advance.

We did not arrive at that approach because it was clever. We arrived at it because it was the only framework that survived contact with a real client’s portfolio of problems. Some problems are solved beautifully by a tool you can adopt on Monday and have in production by Friday, and there is no prize for reinventing capabilities like document summarization or first-pass contract review when excellent commercial products already exist. Other problems, the ones tied to a firm’s particular data and accumulated expertise and unique workflows, are only ever going to be solved well by something built deliberately for that purpose. A mature AI strategy needs room for both, and the organizations making the most progress are the ones that have stopped asking whether they are a build shop or a buy shop and started asking a more useful question instead. For this specific problem, in front of us right now, what is the most advantageous path?

That is the real shift. Build versus buy was a product of its time, and that time has passed. The enterprises pulling ahead are buying to keep up and building to get ahead, treating the combination as the strategy itself and letting the work, rather than orthodoxy, determine the mix.

At Gravity Stack, we continue to test, evaluate, and operationalize emerging AI capabilities so our clients do not have to navigate these decisions alone, from identifying the right tools on the market to building the proprietary solutions that create a genuine edge. If your organization is working through its own build-and-buy strategy, our team is here to help.

👉 If your department is exploring AI, get in touch.

—Follow Gravity Stack on LinkedIn for updates from our AI Lab, client stories, and legal innovation insights.